Summary: In this article, from the graph of major holding companies and it’s main shareholders under Richard Li Tzar Kai, Victor Li Tzar Kuoi, and Li Ka-shing, we found in what areas are they investing and the complex network of relationships between subsidiaries. By analyzing the annual reports of Victor Li Tzar Kuoi and Richard Li Tzar Kai’s company’s companies, we can determine whether Li Ka-shing made the right decision when he announced his retirement.

Background:

Li Ka-shing, a Hong Kong billionaire who will turn 90 this summer, announced his official retirement in May 2018. In January 2015, “Forbes” magazine announced the ranking of Hong Kong’s richest man-Li Ka-shing’s net assets totaled 33.5 billion U.S. dollars, or 260 billion U.S. dollars, making him the richest man in Hong Kong, only replaced by SF Express’s founder Wang Wei in 2017.

He announced on March 16th that he’ll step down as chairman of CK Hutchison Holding Ltd. and CK asset Holding Ltd., making way for his eldest son, Victor Li Tzar Kuoi. Victor assisted Li Ka-shing to run CK holding Ltd. for many years and his youngest son, Richard Li Tzar Kai mainly invested in communications and media business outside.

Richard Li Tzar Kai

We grabbed the information from Who’s Who and HKEX(The Stock Exchange of Hong Kong Limited) and got the name of major holding companies and main shareholder of companies. after establishing their relationship, we got graph below.

Business Map of Richard Li Tzar Kai

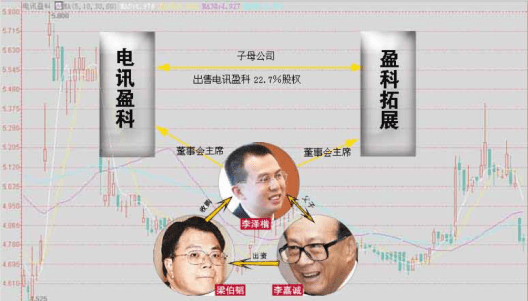

From the graph, we can see that in the case of PCCW limited., which holds Richard Li Tzar Kai as its major shareholder, his father, Li Ka-shing, has also invested in three separate identities, Li Ka-shing Unity Trustee company limited. Li Ka-shing Castle Holdings Limited.and Li Ka-shing Unity Holdings Limited.

It reminded us the PCCW Equity Deal happened in 2006. Richard Li Tzar Kai listed on the empty shell of PCCW Limited. successfully and won the title of “Little Superman” around 2002. After the Internet bubble burst and PCCW’s share price collapsed, he planned to sell PCCW’s core telecommunications and media business to Australia’s Macquarie Group for approximately US$7.3 billion in June 2006. However, it was rejected by China Netcom, the second largest shareholder of PCCW. And then Richard Li Tzar Kai also contacted the consortium led by Francis Leung. he planned to sell 22.65% of PCCW’s shares held by Pacific Century Regional Developments Limited. at HK$9.3 billion in early June.

Behind PCCW: Lee’s Father and Son and Francis Leung

But according to Francis Leung’s list of acquisition consortia announced in November, Li Ka-shing’s acquisition of 12% of PCCW’s shares through its two funds amounted to approximately HK$4.85 billion, and Telefonica received 8% of the shares, while Francis Leung himself holds the remaining 2.65. % of shares.

At that time, Richard Li Tzar Kai was very dissatisfied about the large amount of investment in Francis Leung came from Li Ka-shing.

Richard Li Tzar Kai always hopes to get rid of the influence of Li Ka-shing and chose to start his own business and part-state with the family business. The large amount of investment from Li Ka-shing made him feel that he had not escaped his father’s shadow.

At last, Richard Li Tzar Kai and 76% of the small shareholders of Pacific Century Regional Developments Limited. voted against Francis Leung’s acquisition of PCCW Plan and blocked the previous 22.65% PCCW Equity Interest Sale Agreement with Hong Kong financier Francis Leung.

But what’s interesting is that CK Hutchison Holdings Limited. and Three UK signed a share purchase agreement and invested GBP 300 million (HK$ 2.918 billion) to purchase PCCW’s UK broadband services in 2017.

Total Revenue and Net Profit of PCCW from 2000 to 2016

It can be seen from the announcement of PCCW’s results, The total revenue for 2016 was HK$38.384 billion, a decrease of 2.37% of last year; net profit was HK$2.051 billion, a decrease of 10.63% of last year. Li Ka-shing’s acquisition allowed it to earn nearly 1.3 billion Hong Kong dollars, more than half of the company’s net profit last year.

Although Richard Li Tzar Kai is unwilling to accept help from Li Ka-shing, who does not want to have a dad can shoot 3 billion orders at a crucial moment?

Victor Li Tzar Kuoi

Compared with Richard Li Tzar Kai’s three major holding companies, his brother, Victor Li Tzar Kuoi has more than ten companies, mostly are family business(CK Asset Holdings Limited (KY), CK Hutchison Holdings Limited, CK Infrastructure Holdings Limited (BM), CK LIFE SCIENCES INT’L., (HOLDINGS) INC and Hutchison Whampoa Limited).

Business Map of Victor Li Tzar Kuoi

In 16th March 2018, Li Ka-shing resigned from the company’s chairmanship at the annual general meeting, and his eldest son Victor Li Tzar Kuoi succeed the chairman of the board of directors. However, after Li Ka-shing officially split up in 2012, he explicitly handed over the shares of his 22 listed companies to Victor Li Tzar Kuoi, his youngest son, Richard Li Tzar Kai, who could only obtain cash. Although Li Ka-shing still retains one-third of his interest, almost all decisions are still decided by Victor Li Tzar Kuoi.

Compared to the long-term losses of Richard Li Tzar Kai’s company in recent years, CK Asset Holdings Limited and Hutchison Whampoa Limited Has been continuously profitable. Take CK Infrastructure Holdings Limited.(BM) as an example.

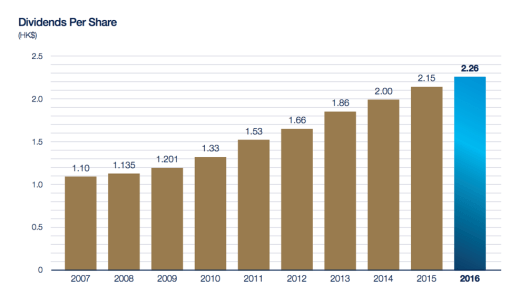

Dividend per Share of CK Infrastructure from 2007 to 2016

The dividends Per share of CK Infrastructure Holdings Limited. has continued to grow since 2007 and achieved the largest increase of 0.2 in 2013.

Because in 2013, Victor Li Tzar Kuoi acquired UK natural gas supplier WWU(Wales & West Gas Networks) for HK$7.753 billion. In addition, during the previous period from 2010 to 2012, CK Infrastructure Holdings Limited. spent a total of 27 billion yuan to complete the acquisition of the UK power grid and the water supply network. From the announcement of CK Infrastructure Holdings Limited.’s results in 2013, the UK business continued to be a major source of profit. In the first half of the year, it recorded a profit of RMB 2.862 billion, but the increase was reduced to 5%. In contrast, profit from investment portfolios in Mainland China and Canada both decreased by 14% to RMB 205 million and RMB 54 million.

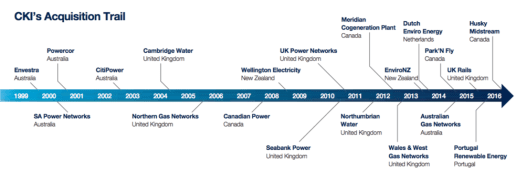

From 2013, CK Infrastructure Holdings Limited. has Continued Expansion of Utilities Business in Europe, after the European debt crisis, the speed of the infrastructure construction of CK Infrastructure Holdings Limited. to Europe and the United States has accelerated.

Investment Portfolio of CK Infrastructure

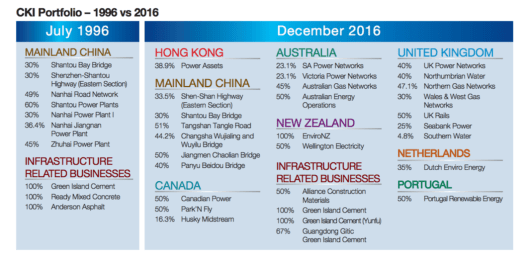

Compared with the CKI portfolio in 1996 and 2016, we can easily concluded that CK Infrastructure Holdings Limited. has shifted their development focus from the mainland to Europe, the Americas and Oceania and infiltrated the local public utilities and achieved obvious success.

Although there is always a small number of people holding views that because of the kidnapping incident, his eldest son will carry most of his family property from Li Ka-shing, We can conclude that Victor Li Tzar Kuoi also has an extraordinary investment perspective in business and the steady and steady spirit that Richard does not possess.

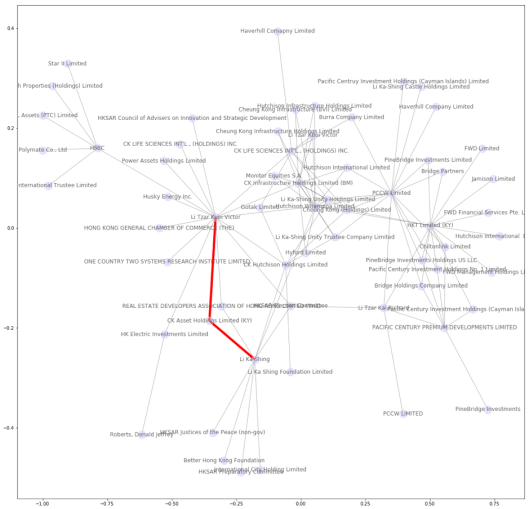

Shortest Path between Li’s Business Map

Shortest Path in Li’s Business Map

Though the shortest path approach, we can check the relationship between two nodes. For example, if we want to know which node connect Li Ka Shing and his big son tightly and directly in business industry(of course not family relationships). We can tell that CK Asset Holding Limited is the node that we want to know.

From this, you can change the code to see other shortest paths between each node, with only changing the codes, which is easy and useful.

Have a Whole Look to Li’s Family Business Map

Li’s Business Empire

This is a whole networking map for Li’s business industry. We can see much information from this graph.

First, from the perspective of company, we can see that the most central point connecting the Li’s family is still Hutchison Whampoa Limited, following with HKT Limited(Hong Kong Telecom), CK Infrastructure Holding Limited. With the analysis of connection denseness, we can have a brief viewing of Li’s family business concentrations.

Second, interestingly, we can see from the graph that Li Ka Shing actually has the least number of connections among the threes Lis. Without a doubt, his old son Li Tzar Kuoi has most connections in business industry with his father’s retirement. Is it because that Li Ka Shing had planned to deliver his power to his older son year before his announcement of retirement? We don’t know but it is definitely worthy that we pay attention and more investigation.

Reference:

- CKI Annual Report 2016

- PCCW Equity Deal

- Victor Li Tzar Kuoi purchase of British natural gas supplier for HK$7.7 billion was called “Buy Britain”

- Richard Li Tzar Kai sells 3 billion yuan of loss-making company, Li Ka-shing to take over.

Codes and data:

Interested readers can download codes and data here: Group 7 – Li’s family business

Notes from lecturer

This group tackled a small graph and tried several variants visualising the graph. The styles are not much different from demo codes and can be further adjusted.

One thing to note in analysing and writing graphs is to keep the same layout across multiple executions. In technical words, safe keep the “pos” variable returned by “spring_layout” (or other layout function), and use the same pos when drawing nodes. Or else, the positions change every time layout algorithm is executed, making it hard to compare those figures in one article.

Another thing is graph analysis is to determine whether the graph is directed or not. In technical words, to handle a directed graph, one needs to use the DiGraph class from networkx. Also in the visualisation part, it is better to draw arrows on the edges to show who points to who. The current case analyses share holding structure, so arrows are essential for people to understand who holds whose share.

Data verification and pre-processing is important. In the first figure, there is one “PCCW Limited” on top which is connected to many subsidiaries. There is also one “PCCW LIMITED” on the left of the graph. It is highly likely the two nodes are the same one.

The discussions, especially the related background of Li’s Family recent moves, are well done and informative. However, more insights could be extracted from the graph analysis/ visualisation and the training of this class expect to see such data-driven insights. For example, in the last figure, one can easily tell that Li Ka Shing and Li Tzar Kuoi are closer, but Li Tzar Kai stands in a relatively separated. This fits the common knowledge that Richard Li Tzar Kai were always trying to setup his own business empire. The article identified that Li Tzar Kuoi had more business connections, but more connections do not mean more business power. One improvement is to enrich the current dataset the market cap and share ratio data. One can visualise market cap using the size of the circles (nodes) and visualise share ratio using the width of the lines (edges). That may give the reader a better picture of business landscape.

— Pili Hu (April 15, 2018)

Author/ Sun Feier; Yu Lei; Yan yang; Hu Zizhe

Editor/ Yucan Xu